Author: Andy Piper

Author: Andy PiperScreening Standards Specialist

ISO 20022 is the global standard for financial messaging, designed to replace legacy formats with richer, more structured data. It enables clearer, more consistent information to be transmitted across payments, supporting improved transparency, automation and compliance.

This blog is the first in a series we’ll be releasing throughout the year exploring the evolution of ISO 20022 and what it means for sanctions screening.

In this first article, as we prepare for the annual Swift changes in November 2026, we’ll take a look at the journey that has brought us this far; in future pieces, we will turn to the November 2026 changes, and what financial institutions should be preparing for in 2027 and beyond.

The evolution of ISO 20022

When asked about ISO 20022, many people will probably think that it’s a relatively new standard. However, it has been around for over 20 years.

Whilst adoption was slow at first, usage became more prominent in Europe following its adoption by the Single European Payment Area (SEPA). Initially utilised for Credit Transfers (2008), this was followed by Direct Debits (2009) and Instant Credit Transfer (2017).

More recently, the last four years have seen a marked increase in adoption since the G20 published its Targets for Enhancing Cross-Border Payments in October 2021. Since then, a range of payment rails and schemes have implemented the standard:

A major step in the adoption of ISO 20022 has been the implementation of Cross-Border Payments and Reporting Plus (CBPR+) by Swift. CBPR+, commonly referred to as MX across the industry, utilises a subset of the larger ISO 20022 guidelines and replaces the historical MT message format.

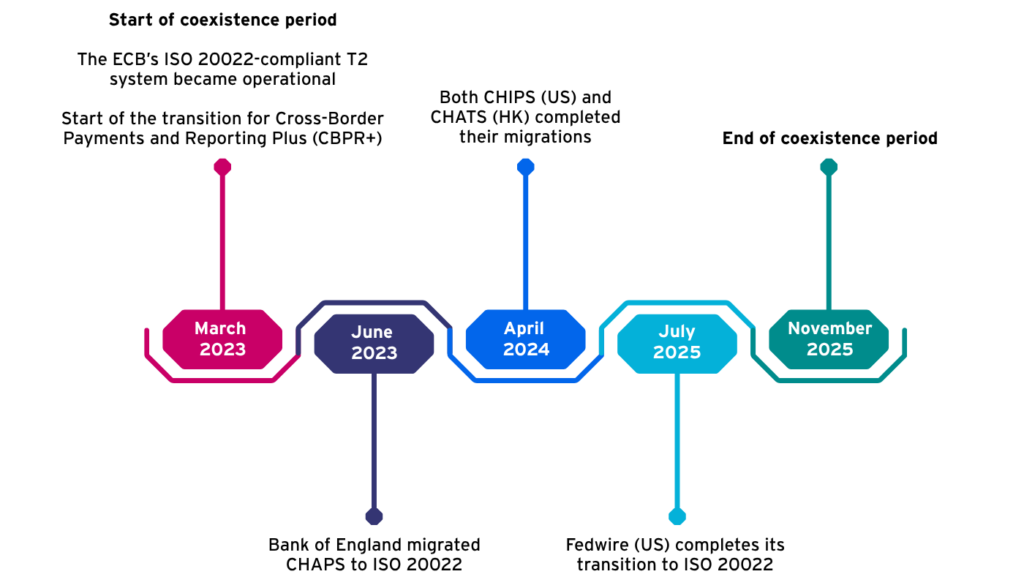

The transition from MT to MX (for cross-border payments) was of course successfully delivered in November 2025, but the journey from inception to completion was years in the making, with one of the key implementation milestones coming in March 2023.

The MT-MX coexistence period (March 2023 – November 2025)

The start of the mandatory transition period for CBPR+ initiated a coexistence period whereby legacy MT messages (including MT103/MT202) and MX formats ran concurrently.

Banks could send both:

- MT (e.g. MT103, MT202)

- MX (e.g. pacs.008, pacs.009)

Banks had to be able to:

- receive MX

- or rely on the Swift translation service (MT → MX)

November 2025: What changed?

A little over six months ago, we reached a significant milestone which was the culmination of years of work from hundreds of financial institutions around the globe. From November 2025, all FI‑to‑FI cross-border payment instructions had to be sent in MX format and the transition for payments was complete.

This meant that:

- pacs.008.001.08 replaced MT103

- pacs.009.001.08 replaced MT202

- pacs.009.001.08(COV) replaced MT202COV

Analysis of Swift traffic from December 2025 has shown just how successful this was. A total of 4.78 million MX transactions were sent/received during the month, representing a significant 97.1% of all payment instructions.[1]

The introduction of ISO 20022 brought with it the opportunity to use structured postal address fields to replace legacy free‑text (MT-style) address lines, with the goal of improving payment transparency, data quality and consistency, thereby enabling more effective sanctions screening.

During the coexistence period the following address formats were supported:

- Fully structured

- Hybrid

- Unstructured

Since November 2025, the options remained the same. However, with the upcoming removal of unstructured addresses in November 2026, the use of fully structured or hybrid addresses (with minimum usage of city/town and country) continues to be strongly encouraged.

Swift analysis from early 2026 suggests there is still some way to go; around 60–65% of payment instructions still rely on unstructured address data, with fully structured formats accounting for less than a quarter and hybrid formats making up a small minority.[2] This highlights the industry still has work to do before structured address data becomes the norm.

How is ISO 20022 expected to improve sanctions screening?

ISO 20022 is expected to bring a range of benefits to sanctions screening, including:

- Data completeness – with larger data fields, the likelihood of data truncation would be all but eliminated, enabling screening to have the richest data possible for alert evaluation.

2. Enhanced entity resolution – through the presence of richer and structured data certain key identifying information such as LEI, birth dates and additional identifiers would be present. With this information within the screening engine, there will be the opportunity to significantly improve the quality of the alerts.

3. Reduced false-positives – with the introduction of structured data, this could arguably become the biggest win for screening. With the engine aware of what fields would hold certain data points, it would enable a field by field (targeted) approach to screening configuration.

Short-term pain, long-term gain

It was always recognised that the implementation of ISO 20022 would be a long and complex journey. Many benefits have already been unlocked but it will take further time to realise the full value.

For data completeness, the capacity to include richer data now exists but it does partly depend on how an institution is storing customer information. If the in-house data is currently limited to fit MT constraints, then we may not be seeing all the expected improvements at this time.

For enhanced entity resolution, the fact that we are now seeing data that was previously not available is providing us with a good baseline for analysis, as we look to refine the opportunities that this brings.

And looking at reduced false-positive rates, the structured data (specifically the splitting of Debtor and Creditor fields) has so far enabled a modest reduction – but with the removal of fully unstructured address fields in 2026 we expect this to increase further.

However, the industry is still limited by the availability of fully unstructured fields in ISO 20022, as were present in MT and which act as a catch-all for any form of data. It remains to be seen whether there will be any change in risk appetite in how these fields are screened.

Talk to us about sanctions screening

At GSS, we have been planning for the ISO 20022 migration since Day One and are ideally placed to unlock the benefits it provides. One example is the way GSS screens every message and field with a bespoke configuration, meaning that the structured data in ISO 20022 is screened precisely in line with the nature of the field in question.

If you’d like to understand how ISO 20022 impacts your sanctions screening process, or explore ways to improve screening effectiveness while reducing false-positives, we’d love to talk to you.

About the author

Andy Piper, Screening Standards Specialist, GSS

Andy has over 20 years’ experience across Tier 1 banking and RegTech, leading large-scale screening transformations and developing data-driven approaches to financial crime risk. As former Group Head of Screening Systems at HSBC, he was responsible for global screening strategy, platform evolution, and regulatory alignment, working closely with regulators, industry bodies, and technology providers. Andy brings deep expertise across sanctions and cross-border risk, screening system design and optimisation, governance, and global operating models, with a recent focus on advancing risk-based, intelligence-led screening approaches.

[1] Swift, ISO 20022 CBPR+ Final Adoption Report (December 2025)

[2] Swift, Removal of unstructured address (accessed June 2026)